Keynesianism and Supply-Side Economics

Keynesianism and Supply-Side Economics

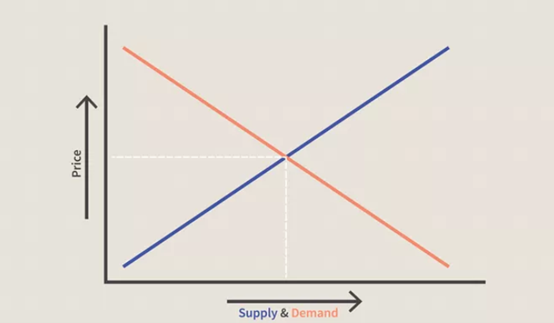

Every time Congress attempts to approve a federal budget, commentators go into full economic nerd mode. They discuss the two elements of any budget at any level — how much money you receive (for governments, that means taxes) and how much money you spend. The chart above is a simple illustration of how prices are set in any economic system — the interaction of supply and demand.

A little explanation is in order. The vertical axis shows price. This particular graph isn’t labeled, but the understanding is that price starts at 0 on the bottom of this axis and increases as it moves toward the top. Numbers are not necessary for a simple understanding of this function. The horizontal axis shows the quantity demanded or supplied. Again, there are no numbers, but 0 is to the left and the quantity increases as you move to the right.

The supply curve (it’s a straight line in this simplified model but economists call it a curve) has a positive slope, up and to the right; this line says “the higher the price, the more suppliers are willing to sell at that price.” That makes sense.

The demand curve (also a straight line) has a negative slope – down and to the right. This line says that “the lower the price, the more buyers are willing to purchase at that price.” Note that this doesn’t say anything about what buyers “want;” in economics, “demand” means “willingness to buy.”

The intersection of these two curves represents market equilibrium: the price at which the quantity suppliers are willing to sell equals the quantity that purchasers are willing to buy. Everyone is happy.

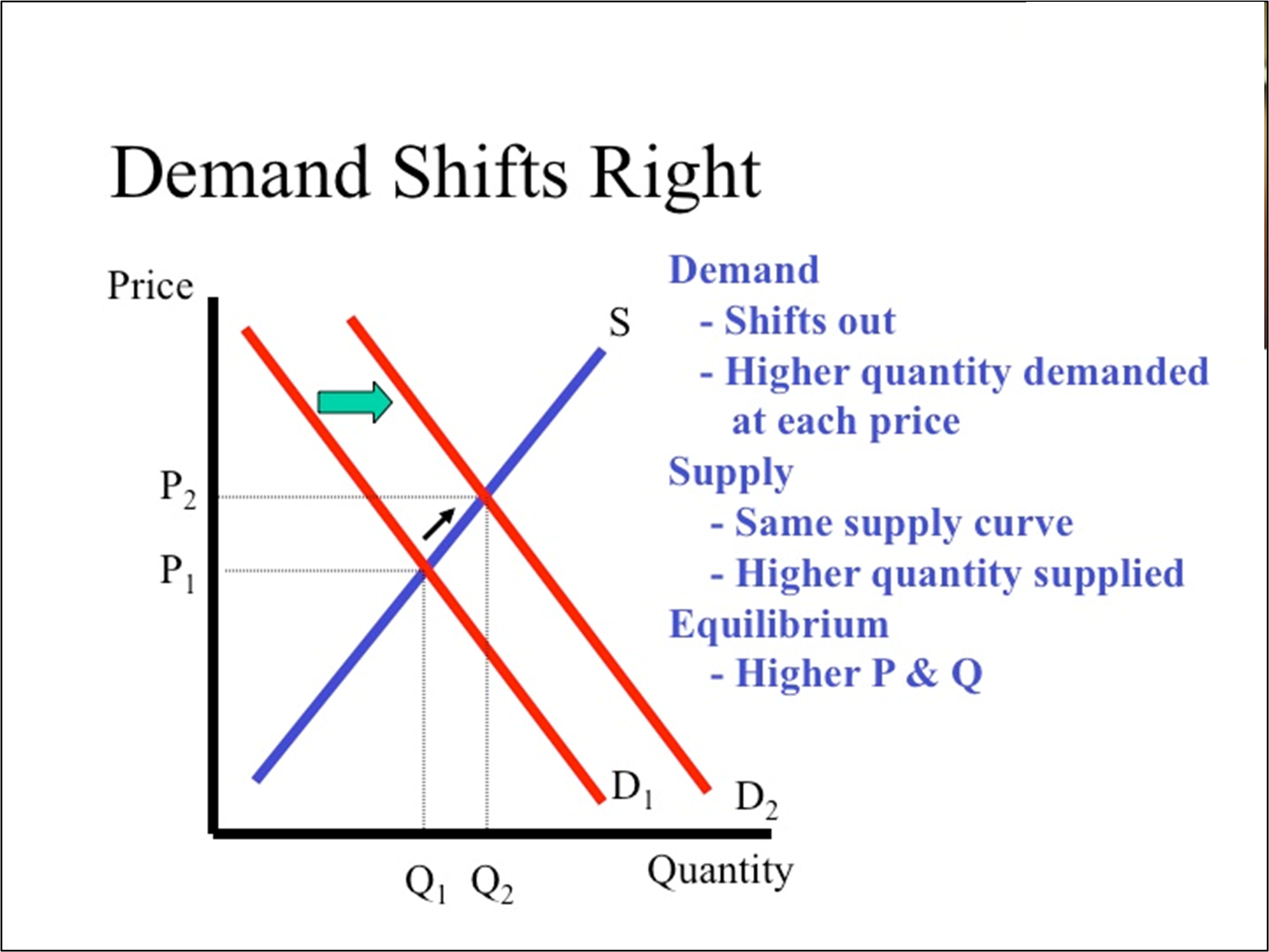

But suppose you are a country, and you want to increase your economic power. This means you want to increase your GDP (Gross Domestic Product) – the total amount of goods and services bought and sold in your country in a year. This means you are unhappy with the place where supply and demand intersect – you want to move it to the right, so that the amount bought and sold increases. How do you do that?

One way is to move the demand curve. This is called “demand-side” or Keynesian economics, after the British economist John Maynard Keynes (pronounced “Canes”) whose theories were popularized in the 1930s. Mainstream politicians of both political parties agreed with the Keynesian approach that said that government spending could play an important role in improving economic health. In 1971, even Republican President Richard Nixon stated that he was a Keynesian.

You improve your economy, say the Keynesians, by making people willing to buy more products at every price level. One way to do this is to give them more money, and, simply speaking, this is the theory that drove American economic policy from the New Deal through the Great Society. This was done through outright cash grants during the New Deal, but also through government spending throughout the economic boom of the 1940s and 1950s. Military spending during World War II created millions of jobs, and those wage earners had more money to spend on consumer goods. In the 1950s, military spending continued to be high (the Cold War) and spending on infrastructure programs (the interstate highway program, housing, and education) put money in people’s pockets as well.

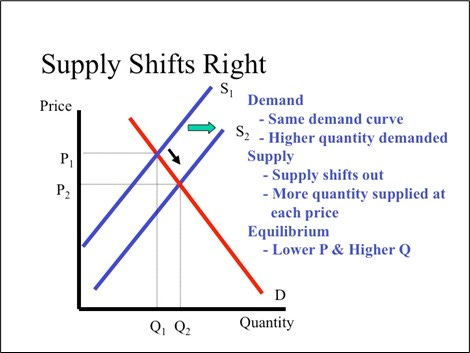

In the 1980s, however, a new idea about economic growth began to circulate. Known as “supply-side” economics, the focus of this theory was still to increase GDP, but this time by shifting the supply curve to the right by increasing the willingness of producers to sell more of their products at a given price level.

What would move the supply curve to the right? If you decrease manufacturing costs (by, oh, say, reducing corporate taxes and eliminating regulations), producers will be able to sell their products at lower prices. That’s good for consumers. Supply-side theory also posits that businesses, with more money in their pockets, will expand their economic activity – building or improving their manufacturing plants, making more of their product, or expanding their market – and that this would create jobs, thus also putting money in the pockets of consumers. A win-win, or so the theory went. The economic benefits of supply-side economics would “trickle down,” and everyone would benefit from greater production at lower prices – unlike Keynesianism, which led to greater production but likely with higher prices.

Sounds great, right? Who wouldn’t like that?

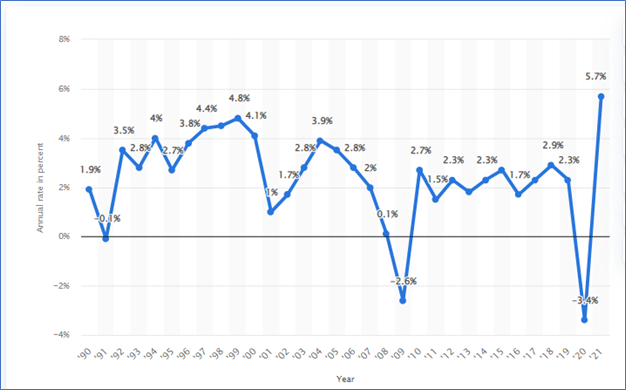

The only problem is that it has never worked. Republicans love supply-side economics and pursue it when they are in a position to do so. This is why when Democrats come into power after a period of Republican rule, their first job always is to save the economy. This graph tells part of the story.

In 1991, the economy was stagnant after two Reagan terms and one Bush I term, where the guiding principle was Supply-Side Economics. The Reagan years saw an economic boom fueled by exploding deficits, as his tax cuts withdrew money from the government but without the “trickle-down” that the theory projected. Deregulation reduced the cost of doing business – but produced the Savings and Loan and Wall Street scandals of his administration His successor, George H. W. Bush, saw the economy continue to falter during his term, leading to a mini-recession in 1991 and his loss of the presidency to Bill Clinton.

Clinton presided over the longest period of peacetime economic expansion in American history, in part by increasing taxes and cutting government spending to reduce the deficits that had plagued both Reagan and Bush. In addition, globalization and technological development spurred economic growth.

When George W. Bush assumed the presidency in 2001, his first legislative priority was tax cutting and deregulation, in line with the 20-year-old GOP supply-side economic strategy.

As we learned in World War II, wars are good for the economy. The decision by the Bush administration to pursue two conflicts – in Iraq and Afghanistan – boosted the economy throughout his term in office. However, by the end of his second term, the United States was experiencing what came to be called the “Great Recession,” as the economy slid and then entered freefall in 2008. All of those supply-side chickens had come home to roost. The first legislative priority by newly elected President Obama was to revive the economy, which he did through an emergency economic stimulus package, Wall Street regulation, and bailouts for the American automobile industry.

When the United States elected Donald Trump to the Presidency, it was clear that a return to supply-side economics lay ahead. The major accomplishment of Trump’s term in office was a tax cut that benefited people at the upper end of the economic spectrum and add substantially to the federal deficit. Coupled with a continued insistence on deregulation, this led to deficits and economic instability.

It’s hard to say how the Trump administration would have ended if there had not been a global pandemic. But the Biden Administration came to office, proposing a wholesale return to Keynesian economics, with four major pieces of legislation – the American Rescue Plan Act, the Infrastructure Investment and Jobs Act, the CHIPS Act, and the Inflation Reduction Act – aimed at stimulating demand and recovering from the economic downturn caused by COVID. President Trump was no longer in office, so we can’t say for sure whether his response to this economic catastrophe would have been to abandon the economic policies he supported while he was in office. But the fact that only a handful of republicans in either the House or the Senate supported any of Biden’s Keynesian legislation suggests that the Republicans, if they had the chance, would take us down the supply-side avenue once again.

How many times will Democrats have to clean up the mess that Republicans make?

ADDENDUM

On Monday, October 10, Robert Reich (noted economist, professor, Cabinet Secretary, economic advisor to President Barack Obama, and a guy much better at this than me) published a Substack newsletter making this same point. Plus his essay includes hyperlinks. This was published after I wrote this essay over the weekend, and I was pleased to see Reich make the same point I was making. Here is Reich’s essay:

Within weeks of taking office, Britain’s new Prime Minister, Liz Truss, and her chancellor of the Exchequer, Kwasi Kwarteng, proposed a radical new set of economic measures that echoed the trickle-down policies of Margaret Thatcher and Ronald Reagan — heavy on tax cuts for the rich and deregulation.

Last Monday, after a backlash from investors, economists, and members of his own party, Mr. Kwarteng reversed one of the proposals, deciding against abolishing the tax rate of 45 percent on the highest earners. But proposals for other tax cuts worth tens of billions of pounds remain intact, as the government insists it is on the right path.

What’s bizarre about this latest episode of trickle-down economics — the abiding faith on the political right that tax cuts and deregulation are good for an economy — is that this gonzo economic theory continues to live on, notwithstanding its repeated failures.

Ever since Reagan and Thatcher first tried them, trickle-down policies have exploded budget deficits and widened inequality. At best, they’ve temporarily increased consumer demand (the opposite of what’s needed during the high inflation that Britain, the US, and much of the world are experiencing).

Reagan’s tax cuts and deregulation at the start of the 1980s were not responsible for America’s rapid growth through the late 1980s. His exorbitant spending (mostly on national defense) fueled a temporary boom that ended in a fierce recession.

Trump’s 2018 tax cut never trickled down.

Yet the US never restored the highest marginal tax rates before Reagan. And deregulation — especially of financial markets — continues to endanger the stability of the economy and expose workers, consumers, and the environment to unnecessary risk.

The result? From 1989 to 2019, typical working families in the United States saw negligible increases in their real (inflation-adjusted) incomes and wealth.

Over the same period, the wealthiest 1 percent of Americans became $29 trillion richer. The national debt exploded. And Wall Street’s takeover of the economy continued.

Meanwhile, and largely as a result, America has become more bitterly divided along the fissures of class and education. Donald Trump didn’t cause this. He exploited it.

The situation in the UK after Thatcher has not been dramatically different.

So why is trickle-down economics still with us? What explains the fatal attraction of this repeatedly failed economic theory?

The easiest answer is that it satisfies politically powerful moneyed interests who want to rake in even more. Armies of lobbyists in Washington, London, and Brussels continuously demand tax cuts and “regulatory relief” for their wealthy patrons.

But why has the public been repeatedly willing to go along with trickle-down economics when nothing ever trickles down? What accounts for the collective amnesia?

Part of the answer is that the moneyed interests have also invested a portion of their gains in an intellectual infrastructure of economists and pundits who continue to promote this failed doctrine — along with institutions that house them, such as, in the US, the Heritage Foundation, Cato Institute, and Club for Growth.

Consider Stephen Moore, the founder and past president of the Club for Growth and a leading economist at the Heritage Foundation, whose columns appear regularly in the Wall Street Journal and is a frequent guest on Fox News.

Moore helped draft and promote Trump’s trickle-down tax. In recent weeks he praised Ms. Truss for her willingness “to challenge the reigning orthodoxy by sharply cutting taxes to boost growth,” calling her package “a gutsy and sound policy decision,” that “will bring jobs, capital and businesses back to the U.K.”

Moore and others like him are happy to disregard the history of trickle-down’s abject failures. They simply repeat the same set of promises made decades ago when Reagan and Thatcher set out to convince the public that trickle-down would work splendidly.

The public has so much else on its mind, and is so confused by the cacophony, that it doesn’t remember — until immediately after the next trickle-down failure.

But perhaps the main reason for the public’s amnesia is that Democrats in the US and Labor in the UK have failed to offer what should be the obvious alternative: A bottom-up economics that invests in the education and health of the public, and the infrastructure connecting them.

This is the only true path to higher productivity and widely-shared prosperity.

Right on. This is a great piece. I hope Reich quotes you. He deserves reading by everyone. I like Reich. (Has a certain ring to it, doesn’t it? )And I always learn good and worthwhile information from you. On economics, I always disagreed with my dad and my late husband. The big bills that have passed in this administration that you reference have thrilled my heart. Let’s lift progressives to the level they need to be for once and for all. For the people.

I shared your essay (and Reich's) with several friends because you made the discussion easy to understand, and I appreciate that. I just bought "Economics for Dummies," but I must be a little below the "dummy" label, because I'm still confused. Thanks again for the writing you do, Karen. It matters.