After Johnny: "Money . . . That’s What I Want"

After Johnny: "Money . . . That’s What I Want"

I’m going to start my essay today by talking about Bitcoin and NFTs (non-fungible tokens), the “new” types of cryptocurrency that are complicating the financial markets. I’ll include a discussion of the recently concluded trial of “crypto king” Sam Bankman-Fried, who is expected to be sentenced to possibly decades in prison for fraud and related crimes.

Confession: I’m lying.

See, I’m not sure what these things actually are. Apparently, they are money but not actually money, confusing the financial markets (and the rest of us) as we try to figure out the world’s increasingly complicated economy.

I suspect a lot of people were in the same quandary in the last decades of the 19th century, as the emerging global industrial economy tried to make sense of money. This was a problem at the time because the various national currencies used different standards for what they called “money,” and this was causing confusion and disruption as goods began to flow more freely around the world as transportation technology and industrialization moved rapidly.

We all know what money is, right? It doesn’t seem like the topic of “money” would generate much political conflict, but an examination of the late 19th century reveals that it was all about money. Not how much money anyone had, but, more fundamentally, what money was.

A little review of monetary theory is in order here, I think.

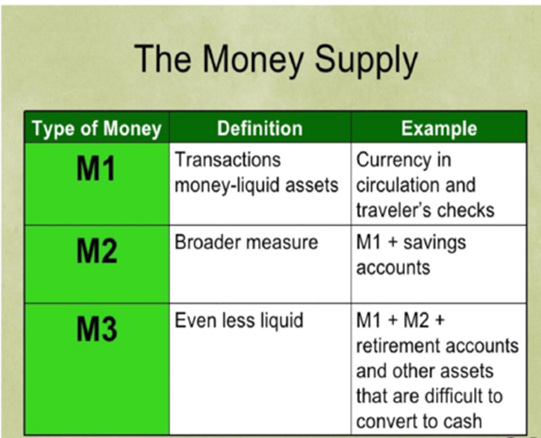

When economists talk about money, they mean the combination of concepts we see in the chart above. I don’t know where crypto fits in the chart. Take a minute to think about all of this.

There are two schools of thought about how to fix the economy of a nation. Proponents of fiscal policy solutions focus on changes in the tax structure in order to expand or restrict the money available to be spent by consumers (including the government) and investors. Proponents of monetary policy solutions believe you can best alter spending and investing by actually expanding or restricting the money supply.

If you want to know more about this, you’ll need to do some research. But this level of understanding is enough for my purposes today.

Between the Civil War and 1900, both politicians and ordinary Americans were obsessed with money – not so much acquiring it and spending it, but more fundamentally understanding what, exactly, it was.

In the preindustrial world, precious metals (gold and silver and occasionally copper) were coined into money because they carried both intrinsic value as a precious metal and representational value as a medium of exchange. Think of this as a kind of expanded barter system, in which people exchanged one thing of value for another thing of value.

It’s hard to emphasize too strongly how much this issue impacted American (and global) economics and politics at the end of the 19th century. I’m working on pulling this apart a little as I prepare for my Osher Class After Johnny next spring.

As industrial growth spurred unprecedented economic expansion, the old ways of doing things – basing “money” on the market value of a specific commodity – no longer sufficed to meet a nation’s economic needs. The United States realized this during the Civil War, as decreased revenues (because of the secession of 11 states) and increased expenses (wars are not cheap) pressed the treasury. The only way to meet the need was to print “greenbacks” – paper notes that carried a government promise to redeem them in hard currency when the war was over. Not surprisingly, people didn’t readily accept this “fiat” money (“fiat” money is money “because the government says so” – the original meaning of fiat in Latin is "let it be done."). When the war was over, holders of greenbacks expected to be repaid in specie – gold and silver.

Here’s where it got complicated. Because gold is rarer than silver, it is more valuable. Unless the market price of gold (think jewelry, for example) maintains a certain ratio to the market price of silver (again, jewelry), speculators will sell one currency, buy the other, and make a profit. The best analogy I can think of today is when travelers exchange one currency for another as they move from one country to another. For example, when the agreed-upon exchange rate increases the value of the dollar, people will exchange dollars to get Euros (for example) that will buy more stuff. That means it’s cheaper for Americans to eat out in Europe than it is for Europeans to eat out in America. And the other way around, also. This is one reason that the European Union created the Euro (a common currency) in the 1990s – to reduce the speculative market in national currencies that was creating financial instability all around.

So here the United States was in 1870 – holders of greenbacks want specie in return, and the government is also eager to withdraw greenbacks from circulation. So no problem, right?

As you have probably guessed, it’s not so simple.

See, gold is still rarer than silver. A gold standard means that there will be less money in circulation. Prices will be stable – little to no inflation. That seems fine, right?

Again, not so simple. Debtors love inflation – this means that the money that they have to pay back – months or years in the future – will be worth less (by the rate of inflation) than the money they borrowed. And as you might expect, lenders and investors hate inflation, for the same reason. This is important politically because this issue becomes a major fissure in the political system. The people who preferred a gold standard (because it would keep inflation to a minimum) coalesced in the Republican Party of post-Civil War America. These are the bankers and industrialists, for the most part. The people who prefer a silver standard (or a bimetal standard – both gold and silver) are the farmers and small businessmen. Farmers, in particular, live on debt. They borrow in the spring to plant their crops or purchase equipment and pay back their debts after the harvest. And they expect to sell their crops at the inflated prices, so that helps them as well. At least, that’s the theory.

This became a raging debate in the 1870s, 1880s, and 1890s, as the United States (along with other industrializing nations) moved back and forth from a gold standard to a silver standard to bimetallism to issuing paper currency again. It is “the” political issue of these decades – every other issue is subsumed under this topic. International trade, labor activism, imperialism, westward expansion, civil rights, urbanization, you name it – they are all impacted by the determination of what, exactly, constitutes money. You can imagine the confusion as everyday people – most of them NOT trained economists, I think it’s fair to say – try to make long-range economic plans. This whole controversy was complicated by discoveries of gold and silver across the West (and across the globe) in the last half of the 19th century. The intrinsic value of gold and silver changed as the supply of the metals changed, increasing uncertainty.

The culmination of this comes in the 1896 Presidential election as Democratic (and Populist) candidate William Jennings Bryant gives his famous “Cross of Gold Speech.” This came after the Democratic Party platform had included a strong statement in favor of bimetallism. Here’s how Bryant ended his speech:

“Having behind us the producing masses of this nation and the world, supported by the commercial interests, the laboring interests, and the toilers everywhere, we will answer their demand for a gold standard by saying to them: "You shall not press down upon the brow of labor this crown of thorns; you shall not crucify mankind upon a cross of gold."

At the end of this speech, Bryant lifted his arms to the side and let his head sag to the front, mimicking a crucifixion. The crowd was silent for several seconds before erupting into cheers. They swarmed to the stage, lifted Bryant onto their shoulders, and carried him around the floor for 25 minutes before order was restored. He won the party nomination – but went down to defeat in the general election a few months later. He won the Democratic Party nomination two more times – in 1900 and 1908 – but never came as close to victory as he had in 1896.

And in case you’re wondering – after reasserting a Gold Standard in 1900, the United States abandoned it (along with most of the nations of the world) during the great depression, and reinstalled (without domestic convertibility) after the 1944 Bretton Woods International Monetary agreement. This meant that countries could keep their reserves in gold as the basis for their currencies, but that the relationship among currencies was fixed in terms of the dollar. International accounts could be settled in gold, but gold was no longer exchangeable in day-to-day commerce. Silver certificates were used as “representative” money between 1878 and 1964. They are no longer being issued, but they still are valid legal tender at their face value.

In 1971, President Richard Nixon famously “floated” the US dollar – meaning that it would no longer be pegged to gold, ending the international convertibility of gold and putting the world on a “fiat” money basis. Today, money is money because we all believe that it is. If we stopped believing that it was money, it would no longer be money.

This, by the way, is one reason why the stability of the United States matters to the world. To the degree that the nations of the world lose confidence in the integrity and efficiency of the US government and economy, they lose faith in the stability of the dollar. If enough countries do this, the role of the dollar in the world could be changed – it could go the way of the gold or silver standard. In a recent meeting between the leaders of Russia and China, one item on the agenda was replacing the dollar with the Chinese currency, the yuan. In 2022, several countries beyond Russia – including Saudi Arabia, Bangladesh, India, Argentina, Brazil, Pakistan, Iraq, and Bolivia – have either traded in the yuan or expressed their willingness to do so in the future.

This stuff matters, my friends.

Most of the Chinese money is invested in US Treasuries because there isn't anyplace else for the Chinese to put their money. So while Russia and other countries have decided to trade in Yuan, they are still trading in dollars. If the Chinese want to continue to sell to the US they will have to continue to buy US Treasuries.

Yikes. Good piece. Though it was different, while reading about money, it immediately made me think about the Depression as being a "correction" or "learning experience" about money. Pretty drastic learning experience, but it does point out the importance of reviewing what things mean and how do we get to where we hope to be. Thanks.